Personal injury settlement taxes depend on what each payment compensates for, not what type of lawsuit produced it. Physical injury compensation, medical reimbursements, and lost wages from a documented physical injury are tax-free under IRC Section 104(a)(2). Punitive damages, settlement interest, and emotional distress without a physical injury basis are fully taxable as ordinary income.

In this blog, we will explain which parts of a personal injury settlement are taxable, and what steps help you report a settlement to reduce taxable income legally.

Key Takeaways

|

Understanding Personal Injury Settlements

A personal injury settlement is money paid to resolve a legal claim for physical harm. Car accidents, slip-and-fall cases, medical malpractice, and workplace injuries all fall under this category.

Settlement payments typically cover:

- Medical expenses from the injury

- Lost wages during recovery

- Pain and suffering

- Emotional distress is tied to the physical injury

- Punitive damages in some cases

How much the IRS takes in taxes from your settlement depends entirely on which of these components your payment covers. Each item carries a different tax treatment.

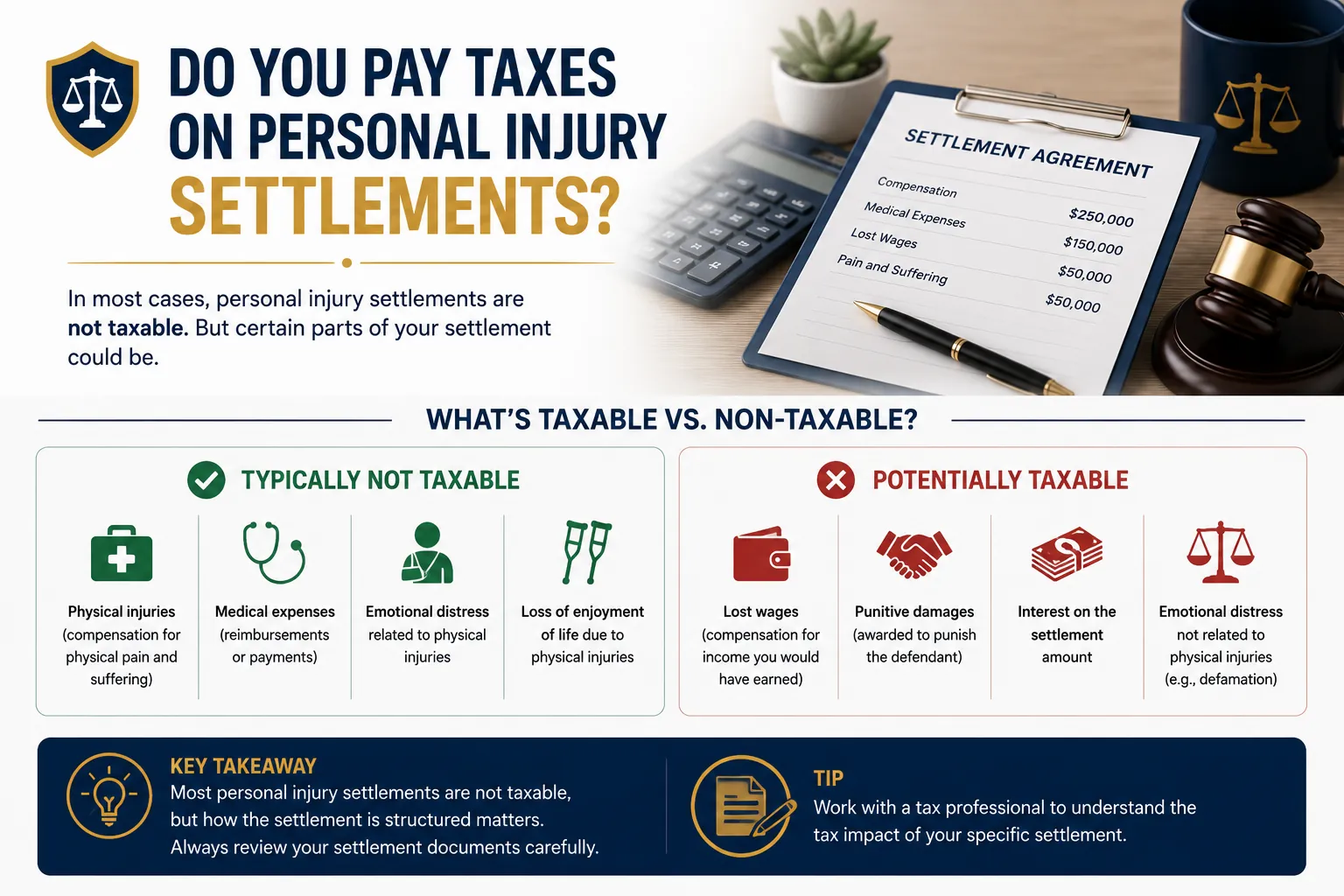

Are Personal Injury Settlements Taxable?

Under IRS Publication 4345 and IRC Section 104, compensation for physical injuries or physical sickness is not taxable. The IRS does not classify physical injury compensation as regular income.

But the exemption has limits. Federal income tax applies to parts of your settlement that fall outside the physical injury category. Punitive damages, interest on delayed payments, and emotional distress without a physical injury basis are all taxable.

The IRS uses the “origin of the claim” rule. Whatever the settlement payment replaces determines the tax treatment.

What Part of the Settlement Is Taxable?

Not the whole settlement. Here is where you pay taxes on personal injury settlements precisely.

Compensatory vs. Punitive Damages

Compensatory damages replace a real loss, such as medical bills, income you could not earn, and pain tied to the injury. The IRS exempts these under IRC Section 104(a)(2).

Punitive damages are entirely different. Courts award punitive damages to punish the defendant. They do not compensate you for an actual loss. The IRS taxes punitive damages in full, even in personal injury cases. Marginal tax rates apply to punitive damages just like regular income.

If your settlement agreement lumps compensatory and punitive damages together without a clear breakdown, the IRS taxes the full amount. Vague agreement language costs you the exemption. The itemization in your agreement protects it.

Medical Expenses and Tax Implications

Medical expense reimbursements are generally not taxable under IRS Publication 525. But one exception gets overlooked constantly.

If you deduct medical expenses on a prior tax return and then receive a settlement covering those same costs, the IRS taxes that reimbursement. This is the tax benefit rule. You claimed the deduction earlier. The settlement repays those costs. The IRS recaptures that earlier tax benefit.

Capital gains taxes also apply when a settlement involves a property or stock transfer. Any gain on the transferred asset is taxable under standard capital gains rules.

Federal income tax does not apply to physical injury compensation at all. But punitive damages push your taxable income higher, which can move you into a worse tax bracket.

When Are Personal Injury Settlements Not Taxable?

You don’t pay taxes on personal injury settlements when the settlement compensates for physical bodily injury or physical sickness under IRC Section 104 and IRS Topic No. 160.

These payments qualify as non-taxable settlement proceeds:

- Compensation for physical bodily injury or illness

- Medical bill reimbursements from the injury (if not previously deducted)

- Lost wages resulting directly from the physical injury

- Emotional distress arising directly from a documented physical injury

- Workers’ compensation for a physical injury

Your settlement agreement must clearly state that the payment is for physical injury. Vague language gives the IRS authority to reclassify the payment as taxable. Your attorney should document this before you sign anything.

Reducing taxable income with deductions applies in specific cases where portions of the settlement are taxable. Whistleblower and employment discrimination legal fees are deductible above the line. Personal injury legal fees are not deductible under the post-2017 law.

How to Report Your Personal Injury Settlement Income

If you pay taxes on personal injury settlements, you need to know where each piece goes on your tax return. Form 1040 reporting for settlement income works like this:

- Punitive damages: Report on Schedule 1, Line 8 as “other income.”

- Interest on settlement payments: Report on Schedule B as interest income

- Employment-related settlement components: Report on Line 1 using your W-2 or 1099

- Non-taxable physical injury compensation: Not reported at all

Large taxable settlement amounts require estimated taxes paid quarterly. The IRS expects these payments when your tax bill exceeds $1,000 for the year. Missing them triggers an underpayment penalty.

Common Mistakes in Reporting Personal Injury Settlements

Most settlement recipients have no experience with what the IRS takes in taxes on legal awards. That gap creates mistakes that cost real money.

Common tax filing mistakes with personal injury settlements include:

- Not separating punitive from compensatory damages: A single lump-sum settlement without a clear breakdown gives the IRS room to tax everything.

- Missing interest income: Interest on delayed settlement payments is taxable. It often gets left off the return entirely.

- Ignoring the tax benefit rule: If you previously deducted medical costs and received reimbursement, that amount is taxable. Skipping this causes CP2000 notices from the IRS.

- Assuming all emotional distress is non-taxable: Only emotional distress tied directly to a physical injury is exempt. Without that documented link, the IRS taxes it as ordinary income.

- Skipping estimated tax payments: Large taxable portions create obligations that regular W-2 withholding does not cover.

Reducing tax liability through correct settlement classification and clear agreement language prevents most of these mistakes before filing day.

When to Consult a Tax Professional with Taxes on Settlements

If you pay taxes on personal injury settlements that include punitive damages, property transfers, or emotional distress components, that is when a tax professional stops being optional.

Consult one when:

- Your settlement includes punitive damages

- You previously deducted medical expenses; the settlement covers

- Your settlement involves property, stocks, or other assets

- The settlement amount pushes you into a higher tax bracket

- Your agreement does not clearly distinguish between taxable and non-taxable amounts

High-income tax strategies apply directly to large settlements. Spreading taxable payments across multiple tax years keeps you within lower marginal tax rates. This approach is legal and widely used for large awards.

In our practice at SWAT Advisors, the single most preventable mistake we see is clients signing settlement agreements with vague damage language. Once you sign, the IRS has the authority to tax the full amount. Getting the classification right before you sign costs nothing.

File Settlement Taxes Right With SWAT Advisors

If you pay taxes on personal injury settlements and feel like you are guessing your way through IRS rules, SWAT Advisors provides specific, accurate settlement tax guidance for individuals across the United States.

Our team helps individuals review settlement agreements, identify taxable and non-taxable components, structure settlements strategically, and implement proactive tax planning strategies that hold up under IRS scrutiny.

SWAT Advisors can help you reduce tax exposure before filing mistakes become expensive problems. Contact us today to build a smarter settlement tax strategy with confidence.

FAQs

No. The IRS exempts compensatory damages for physical bodily injury and sickness under IRC Section 104(a)(2). Punitive damages, settlement interest, and emotional distress without a physical injury basis are taxable.

IRS Publication 4345 exempts physical injury compensation, physical sickness damages, medical reimbursements from a physical injury (if not previously deducted), lost wages from the physical injury, and emotional distress arising directly from that same physical injury.

It depends on the source. Pain and suffering directly tied to a physical injury is tax-exempt. Pain and suffering from emotional distress alone, with no documented physical injury, is taxable as ordinary income.

Punitive damages go on Schedule 1, Line 8 of Form 1040. Settlement interest goes on Schedule B. Physical injury compensation does not get reported at all.

Yes, whenever your settlement includes punitive damages, property transfers, or medical costs, you previously deducted. When you pay taxes on personal injury settlements with multiple damage types, a tax professional prevents misclassification errors before they become IRS audits.

{kind=link}

{kind=link}