Latest Facts and News

- According to PwC’s 2021 Family Business Survey, only 34% of family businesses have a robust, documented succession plan.

- The COVID-19 pandemic has accelerated succession planning discussions in many family businesses.

- Recent studies show that only 30% of family businesses survive into the second generation, highlighting the importance of proper succession planning.

- Family businesses contribute to 70–90% of global GDP annually, emphasizing their economic significance.

Your family business represents generations of effort, dedication, and shared dreams. It’s a reflection of your family’s hard work and values, a legacy that deserves to be preserved and nurtured.

Family business succession planning is what guarantees this legacy to continue thriving, not just for the next generation but for many more to come.

A strong plan comes when the person leading is prepared, capable, and aligned with the business’s vision. Simultaneously, it’s equally important to recognize that leadership alone isn’t enough—the involvement of clear processes and open communication among all stakeholders is also an important step in the generational transition.

This blog post will cover everything that can make your family business transition smooth, ensuring its stability, growth, and business continuity for future generations. Hold that thought because we’re not just talking about leadership here; we’re moving into the strategies, tools, and insights that will help you secure your family’s legacy for years to come.

Understanding Family Business Succession Planning

Family business succession planning involves preparing the next generation for leadership and ownership roles in the family business.

It is like laying the groundwork for the future, ensuring that the business runs smoothly and the family legacy continues to thrive.

When you plan ahead, it helps avoid any drama or confusion and makes the whole process feel natural, keeping the business growing and thriving.

Importance of Family Business Succession Planning

Succession planning is what keeps a family business steady and thriving in the long run. Here’s why it’s so important:

- Ensures Long-Term Stability: A good succession plan helps to establish a long-term structure for the business, allowing it to grow and adapt as it passes through different generations.

- Encourages Entrepreneurship: It allows family members to step forward, think outside the box, and actively contribute to the business’s success.

- Prepares Future Leaders: The next generation gets hands-on experience and guidance, so they’re ready and confident when it’s their time to lead.

- Brings the Family Closer: When everyone works toward the same goals, it builds teamwork, encourages joint decision-making, and strengthens family ties.

- Boosts the Business’s Value: With a clear plan in place, the business becomes stronger and more innovative, inspiring family members to stay invested and bring their best ideas forward.

- Adds Fresh Perspectives: The younger generation often brings new ideas that can update strategies and keep the business relevant in a changing world.

- Takes Away Uncertainty: Having everything mapped out means no confusion or hesitation about the future, keeping the business running smoothly no matter what.

Key Components of a Successful Succession Plan

A good succession plan addresses some primary issues to ensure that everything runs smoothly when it comes time to pass the baton. Let’s take a quick look:

- Identifying and Preparing Leaders: Start by finding the right people to take over key roles. Whether it’s family members or trusted team members, focus on building their skills and getting them ready for leadership.

- Creating a Timeline: A clear timeline helps everyone know what steps to take and when. It keeps things organized and makes the transition easier for everyone involved.

- Handling Financial and Legal Details: Taxes, ownership transfers, and legal requirements need attention to avoid complications. Getting these details in place ensures a smooth process.

We’ll go into more detail about each of these steps in the sections below. You’ll find simple, clear explanations and practical tips to help you get through the process, prepare for the future, and ensure your business is ready for a smooth and successful transition.

The Importance of Early Succession Planning

Starting family business succession planning early is one of the best decisions a family business can make. It gives everyone enough time to prepare for the future and make smart, thoughtful choices. Here’s why it matters:

- Time to Find the Right Successor: When you start early, you can carefully look at potential successors and see who’s ready to lead. This also gives time to help them learn and grow into the role.

- Avoid Last-Minute Stress: Planning ahead means you don’t have to rush into decisions. Rushed choices can lead to mistakes that might hurt the business.

- Build a Strong Future: Early planning isn’t just about the next leader—it’s about setting the business up for success for years to come. It ensures the company continues to grow and thrive for future generations.

Taking the time to plan now makes the transition smoother for everyone and keeps the business steady and successful.

How to Start Early: A Succession Planning Timeline

To make early family business succession planning actionable, it’s essential to follow a structured timeline. Here’s a recommended timeline to guide your family business through the succession process:

| Timeline | Actions |

| 5–10 years prior | Identify potential successors and start leadership development. |

| 3–5 years prior | Formalize the succession planning process; address legal and tax considerations. |

| 1–3 years prior | Increase successor responsibilities and communicate the succession plan. |

| Final year | Execute the transition, step back from daily operations, and support new leadership. |

Using this timeline can address key steps gradually and avoid last-minute stress. It ensures that successor preparation is done right, stakeholders are informed, and the business is set up for a seamless transition.

Developing the Next Generation of Leaders

Preparing the next generation of leaders in a family business goes beyond simply choosing the next CEO. It’s about identifying the right candidates, helping them grow, and mentoring them to lead effectively.

Here’s a simple guide to make this process easier:

1. Identify the Right Potential

Look for family members who show promise, not just based on past successes but on traits that matter for leadership. Focus on qualities like:

- Self-awareness: Do they understand their strengths and areas for growth?

- Adaptability: Can they handle challenges and adjust to changes?

- Relational skills: Are they good at building connections and fostering teamwork?

| Actionable Tip: Regularly assess potential candidates and have open discussions to identify who is genuinely interested and capable. |

2. Focus on Vertical Development

Horizontal development (learning new skills) is important, but vertical development (personal growth and deeper self-reflection) is what shapes great leaders. This process encourages future leaders to:

- Reflect on their goals and how they align with the business.

- Understand how their decisions will impact the organization.

- Balance personal life with leadership responsibilities.

| Actionable Tip: Start leadership development 1.5–2 years before any planned transition to allow enough time for growth. |

3. Provide Mentorship and Guidance

Mentorship plays a critical role in preparing the next generation. Pair potential leaders with experienced mentors to help them navigate challenges, gain hands-on experience, and build confidence.

- Involve them in key business decisions.

- Create opportunities for them to lead small projects.

- Encourage self-reflection through feedback and regular discussions.

| Actionable Tip: Set up structured mentoring programs within the family business to provide ongoing support and learning. |

Legal and Financial Considerations in Family Business Succession

Creating a clear and structured succession plan involves addressing both legal and financial aspects. Below is a straightforward guide to the key considerations:

Legal Considerations Checklist

- Estate Planning

- Estate planning involves draft wills to specify how business assets will be distributed.

- Establish trusts to protect ownership and facilitate smooth transfers to beneficiaries.

- Create buy-sell agreements to define ownership transfer terms during events like death, disability, or retirement.

- Tax Planning

- The main goal of tax planning is to minimize tax liabilities by including gift and estate taxes through strategic preparation.

- Stay compliant with federal and state tax regulations to avoid penalties.

- Buy-Sell Agreements

- Ensure agreements include terms for valuation and ownership transfer in specific situations like retirement or death.

- Define clear procedures to prevent conflicts during transitions.

- Confidentiality and Non-Compete Agreements

- Protect sensitive business information, including trade secrets and customer lists, with confidentiality agreements.

- Draft non-compete agreements to prevent outgoing employees or owners from competing with the business.

- Compliance with Regulations

- Review and adhere to state and federal laws, including tax, employment, and securities regulations.

- Consult legal experts at SWAT Advisors to ensure all documents are compliant and enforceable.

Financial Considerations Checklist

- Debt Management

- Review existing debt obligations, including personal guarantees.

- Negotiate with creditors to avoid liabilities that could hinder the transition.

- Cash Flow Stability

- Analyze operating and free cash flow trends to ensure financial health.

- Address any volatility to maintain a strong business valuation.

- Long-Term Financial Modeling

- Develop a comprehensive 5–10 year financial plan, including profit and loss statements, balance sheets, and cash flow projections.

- Conduct risk assessments to anticipate potential challenges and develop solutions.

- Taxes and Transfer Costs

- Calculate personal tax liabilities, asset transfer taxes, and legal fees.

- Plan for expenses like owner compensation replacement and key employee incentives.

Know More→ Family Business Success Strategies: Navigate With Experts

Communicating the Succession Plan to Stakeholders

Effective communication is an important part of any succession plan. It ensures that everyone impacted by the transition understands the plan, feels reassured, and remains aligned with the business’s goals. Here’s how to address key stakeholder groups:

- Family Members and Shareholders

Family members and shareholders often have a direct stake in the business.

- Be Transparent: Share the succession plan early to avoid misunderstandings.

- Clarify Roles: Clearly define responsibilities and how the transition aligns with the company’s vision.

- Employees

Employees need to feel confident in the leadership transition to maintain morale and productivity.

- Communicate Early: Inform them about the plan to prevent rumors.

- Highlight Growth Opportunities: Explain how the transition may create new roles or training opportunities.

- Clients and Business Partners

Stakeholders outside the business, such as clients, suppliers, and partners, rely on consistency.

- Provide Reassurance: Let them know the leadership change won’t affect the quality of services or operations.

- Share Key Updates: Inform them of any changes that may impact their engagement with the business.

Keeping everyone in the loop during a leadership transition helps maintain stability and trust across the organization. Clear and consistent communication ensures that stakeholders feel confident, understand what to expect, and remain aligned with the company’s goals.

Bonus→ Expert Succession Planning Services | Business & Family

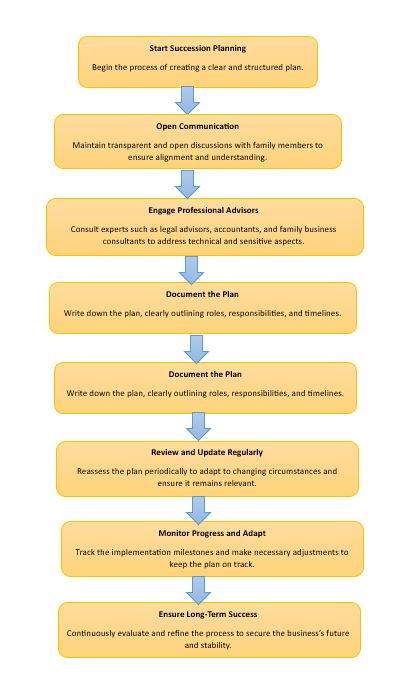

Best Practices for Implementing Monitoring the Succession Plan

Securing Your Family Business Legacy

Your family business represents years of dedication, vision, and hard work. Ensuring its future requires careful family business succession planning to protect what has been built and to prepare for the opportunities and challenges ahead. Laying a strong foundation ensures the business remains steady and thrives for generations to come.

At SWAT Advisors, we can guide you through every step of the family business succession planning process with expertise and care.

- We simplify the process by helping you map out clear steps, tailored timelines, and actionable strategies for leadership transitions.

- We address sensitive family dynamics with transparency and care, ensuring open communication and alignment among all stakeholders.

- Our experts handle the technical aspects, from estate planning and tax management to creating robust legal frameworks that secure the future of your business.

With the right plan in place, you can move forward confidently, knowing your family business is ready for the future. Reach out to SWAT Advisors today and let’s start building your lasting legacy.

Also Read About→ Business Continuity Planning for Modern Enterprises

FAQ's

The time it takes to develop a family business succession plan can vary greatly. For some families, it might take a few months, while for others, it can stretch into several years. The process often depends on factors like the size of the business, the complexity of ownership, and how prepared the potential successors are.

With SWAT Advisors by your side, you have someone who knows everything from mapping out clear steps to handling sensitive family dynamics and an expert team who understands the technical details. This can make the process as less time-consuming as possible, ensuring a smoother and more efficient transition.

Family business successions often fail due to common challenges, including:

- Unresolved family conflicts that damage trust.

- Successors lack interest in taking over the business.

- No clear exit plan for the current owner.

- Inadequate training for the next generation.

- Misunderstandings about ownership, such as assuming the business will be inherited.

These challenges don’t have to define the future of your family business.

We understand the root cause of these issues and the lack of interest because we have dealt with such things already. But there are solutions that can be used. We can help you understand the situation and the solutions so you can figure out what is best for you.

Yes, a family business succession plan can absolutely include non-family members. It’s all about choosing the right leader, whether they’re part of the family or not.

The process involves:

- Identifying potential successors based on skills and leadership qualities.

- Providing mentorship and training to prepare them for their roles.

- Establishing clear roles and responsibilities to ensure a smooth transition.

- Maintaining open communication with family members and stakeholders.

Choosing the best leader, whether family or not, helps ensure the business continues to thrive.

A family business succession plan should be reviewed every few years. As the business grows and circumstances change, regular updates ensure the plan stays relevant and aligned with new goals or challenges.

Get in touch with SWAT Advisors to get the best services for reviewing and updating your family business succession plan.

Family governance structures create a solid foundation for smooth leadership transitions and long-term success. They provide clarity in key areas, ensuring the business operates seamlessly through generations.

- Clear Ownership Roles: Define responsibilities for all family members, reducing confusion.

- Decision-Making Framework: Establish processes to guide business decisions and resolve conflicts.

- Open Communication: Foster transparency and align family values with business goals.

With this framework, businesses can avoid misunderstandings, maintain continuity, and ensure a successful transition to the next generation.

{kind=link}

{kind=link}