Latest Facts and News

- The Illinois Department of Insurance recently highlighted benefits for small businesses resulting from national health reform.

- Small businesses in Illinois can now access tax credits of up to 35% of premium costs for providing health coverage to employees.

- The state has implemented measures to protect small businesses against dramatic premium increases and ensure better value for insurance dollars.

Illinois is home to small businesses numbering 1.2 million. These small businesses account for 99.6% of the whole business and employ close to 45% of the workforce in the entire state. As a matter of fact, small businesses entrenched themselves very strongly with an important subsequent role in the economy, carrying with them the risks that could threaten business stability.

Any damage ranging from a minor lawsuit or damage to business property to an unforeseen liability that ends up generating a financial loss cannot be ignored. Therefore, appropriate insurance should be carried in this regard.

Therefore, small business insurance in Illinois gets its much-deserved attention. Such insurance will provide you protection for your business in case you find yourself in the courtroom contesting something.

This blog post highlights the Illinois business insurance coverages (also known as Prairie State business coverages) mandated by law, the essentials of protective policies, together with the concept of cost for incorporation later on, thereby aiding somebody in breaking down informed choices for the company’s stability.

Understanding Small Business Insurance Requirements in Illinois

Having an understanding of small business insurance requirements in Illinois can protect you as well as your business and employees.

Illinois law requires certain types of coverage, such as workers’ compensation and unemployment insurance, while others, like general and professional liability insurance, are optional but offer valuable protection against litigation, property damage, and financial risks. We’ll cover these in detail later.

First, let’s take a closer look at the mandatory insurance requirements:

Workers’ Compensation Insurance

Workers’ compensation insurance is essential for small businesses in Illinois. The state mandates that all businesses that have employees, including part-timers, must provide compensation for the workers.

It ensures employees are compensated for:

- Medical expenses

2. Lost wages - Rehabilitation costs if injured on the job

4. Disability benefits

5. Death Benefits

According to the US Bureau of Labor Statistics, there were around 101,400 non-fatal injuries and illnesses occurring at the workplaces of private companies in Illinois in 2023. Therefore, you will have to carry workers’ compensation insurance in order to avoid severe penalties and legal implications.

Unemployment Insurance

Unemployment insurance is another mandatory obligation for Illinois companies that have employees. This insurance offers monetary support to workers who are terminated from their positions due to layoffs or other eligible causes.

It is funded through employer contributions, the amount of which is specified as a percentage of workers’ salaries. The Illinois Department of Employment Security leads the program with oversight and benefit payouts.

Here is How It Works→

- Employers finance the program by contributing a portion of their employees’ wages as payroll taxes.

- IDES administers unemployment claims, ensuring that eligible individuals receive benefits.

- Qualified employees can receive benefits for up to 26 weeks within one year, depending on when their claim was established.

To find details on unemployment insurance requirements in Illinois, you can visit the Illinois Department of Employment Security’s website.

Essential Small Business Insurance Coverages in Illinois

Small-scale business owners must possess some important business insurance coverages in Illinois. Certain suggested insurance categories for small businesses include general liability and professional liability.

Let’s discuss them in more detail:

General Liability Insurance

This is among the fundamental small business insurance in Illinois, and it offers you coverage on the following:

- Injury: If anyone is injured at your business premises, then medical expenses can be covered.

- Damage to property: In case of damage done by your business to a third party’s property, payment will be made.

- Legal defense: Covers attorney fees and court costs if you’re sued.

Professional Liability Insurance

Professional liability insurance (also called errors and omissions insurance) is a must-have for all those who have a service-based business in Illinois. It protects against claims of negligence or mistakes in your professional services.

It provides coverage for:

- Errors or omissions in service delivery.

- Misrepresentation or breach of contract.

- Damages arising from incorrect advice.

This coverage is especially critical for industries like consulting, legal services, and healthcare, where precision is paramount.

Small Business Health Insurance Options in Illinois

Health insurance is one of the most important aspects of small business insurance in Illinois, as it directly impacts employee satisfaction and legal compliance. Understanding the small business health insurance Illinois options available can help you offer the right coverage while managing costs effectively.

Group Health Insurance Plans

Small business group health insurance Illinois enables small businesses to offer healthcare coverage to employees at competitive rates. In Illinois, businesses with 2 to 50 employees can access these plans through providers like Blue Cross and Blue Shield of Illinois, which offer flexible solutions to small businesses as:

- Enhanced employee retention.

- Lower rates compared to individual plans.

- Compliance with state and federal laws.

Small businesses may qualify for the Small Business Health Care Tax Credit, which covers up to 50% of premium costs for employers who provide health insurance to employees.

Also Read-> Taking Care of What Matters: A Simple Approach to Estate Planning

Health Savings Accounts (HSAs) and Health Reimbursement Arrangements (HRAs)

HSAs and HRAs are small business health insurance alternatives that provide tax-advantaged ways to manage healthcare costs.

Below is a comparison table: HSA vs. HRA for a better understanding:

| Feature | Health Savings Account (HSA) | Health Reimbursement Arrangement (HRA) |

| Definition | A savings account owned by the employee to pay for qualified medical expenses. | An employer-funded arrangement that reimburses employees for qualified medical expenses. |

| Ownership | Owned by the employee; funds stay with the employee even after leaving the job. | Owned by the employer; unused funds typically revert to the employer after employment ends. |

| Funding | Contributions made by the employee, employer, or both. | Funded solely by the employer. |

| Eligibility | Requires enrollment in a high-deductible health plan (HDHP). | Does not require HDHP enrollment, but eligibility and rules are set by the employer. |

| Tax Advantages | Contributions are pre-tax or tax-deductible, and withdrawals for qualified expenses are tax-free. | Reimbursements for qualified expenses are tax-free to the employee. |

| Qualified Expenses | Medical, dental, vision, and some over-the-counter expenses (as defined by the IRS). | Medical, dental, vision, and other qualified expenses as defined by the employer. |

| Portability | Fully portable; funds remain with the employee regardless of employment status. | Not portable; funds remain with the employer. |

| Roll-Over Funds | Unused funds roll over from year to year and can be invested. | Employers may allow unused funds to roll over, but this is not mandatory. |

Note: These plans are often combined with high-deductible health plans (HDHPs) to offer cost-effective and flexible coverage, allowing businesses to manage expenses while still providing essential small company health benefits.

Cost of Small Business Insurance in Illinois

The cost of small business insurance in Illinois varies based on factors such as industry, location, number of employees, and coverage types.

For instance, the average cost of a general liability insurance policy is $42 per month or $500 per year for small businesses.

It is advisable to obtain quotes from multiple providers to compare rates and coverage options to get the best affordable business coverage in Illinois.

Factors Affecting Insurance CostsFive factors usually affect the rates of small business insurance in Illinois. These are: |

Tips for Reducing Insurance Premiums→

|

Top Small Business Insurance Providers in Illinois

Choosing the best small business insurance in Illinois depends on your specific needs. Whether you’re looking for industry-specific coverage, the convenience of comparing multiple quotes, or affordable and customizable plans, these providers offer the best options to make sure your business is properly covered.

Below is the comparison table of top entrepreneur insurance options:

| Provider | Coverage Types | Key Features |

| The Hartford | General Liability Property Workers’ Compensation | Tailored industry-specific coverage risk management tools 24/7 customer service |

| Insureon | General Liability Property Professional Liability | Compare quotes from multiple insurers Simple online application |

| NEXT Insurance | General Liability Professional Liability Property | Affordable rates Customizable policies No broker fees |

| Progressive Commercial | General Liability Auto Insurance Property | Flexible coverage Competitive Pricing 24/7 claims service |

Small Business Insurance in Illinois for LLCs

Forming an LLC helps protect personal assets, but it doesn’t shield the business itself from financial risks. Without the right insurance, lawsuits, property damage, or employee-related claims could result in significant out-of-pocket expenses.

Key insurance coverages for LLCs in Illinois include:

- General Liability Insurance: Covers third-party claims for bodily injury, property damage, and legal costs. Essential for protecting against unexpected lawsuits.

- Professional Liability Insurance: Protects service-based businesses from claims of negligence, errors, or omissions in their work.

- Workers’ Compensation Insurance: Mandatory in Illinois for businesses with employees. Covers medical expenses and lost wages for work-related injuries.

Having the right coverage ensures that your LLC stays protected from costly claims while maintaining financial stability.

Read More-> Small Business Exit Mastery: Your Comprehensive Guide

Steps to Obtain Small Business Insurance in Illinois

If you run a small business in Illinois, the steps below will guide you in purchasing the right insurance coverage:

- Get to Know the Types of Business Insurance: Familiarize yourself with the different insurance policies needed for your business, such as general liability, professional liability, and property insurance.

- Assess Your Risks: Identify potential risks associated with your business to choose appropriate coverage that mitigates those specific threats.

- Obtain Quotes and Compare Them: Check with different insurance companies to get quotes and compare their options and prices. This way, you can make sure you find the best deal for your money.

- Look for Policy Exclusions and Limits: Carefully review what each policy covers and excludes, as well as the coverage limits, to avoid unexpected gaps in protection.

- Choose a Reputable Insurance Provider: Look for a company that is easy to work with, has a solid credit score, and gets fair reviews from customers when they need to make claims.

- Look at Deductibles: If you choose a higher deductible, your premium rates might go down. But make sure your business can pay that deductible if you ever have to make a claim.

- Seek Professional Help: Insurance agents and brokers can be a great resource to offer advice specific to your business and its unique needs.

- Regularly Reassess Your Coverage: As businesses expand, they go through various changes, so it’s important to frequently review and update their insurance coverage to match those changes.

Protect Your Business Future with SWAT Advisors!

You can’t risk your business and assets as a small business entrepreneur. Illinois startup protection plans and insurance coverage are an investment in your small business’s future.

Now that you know about the importance of small business insurance in Illinois, the options available, and the steps to obtain it, you are just one step away from protecting your business by taking action.

If you need personalized advice or complete solutions, think about contacting SWAT Advisors. They focus on assisting small business owners in Illinois and nationwide with the insurance process, making sure you receive the necessary coverage at a competitive price.

Get in touch today!

FAQ's

In Illinois, the minimum small business insurance required for employees is the workers’ compensation insurance to cover workplace injuries, illnesses, and disability benefits. Also, businesses that use vehicles must carry Illinois commercial insurance.

Then, there is general liability insurance, which is not legally required but is strongly recommended to protect against common risks.

In Illinois, small business health insurance can start for as little as about $111 per employee. However, the pricing will vary based on several factors, including the number of employees, gender, age, and tobacco use.

You can get free quotes from eHealth and compare plans to find the best coverage options for you and your employees.

Definitely. Many small business insurance providers like Insureon, Hartfort, and NEXTInsurance allow business owners to obtain quotes, compare coverage options, and purchase insurance online. These platforms offer customized plans based on your industry, coverage needs, and budget.

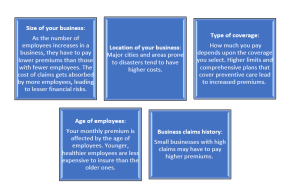

- There are five factors that usually affect small business insurance rates in Illinois. These are:

- Size of your business: As the number of employees increases in a business, they have to pay lower premiums than those with fewer employees. The cost of claims gets absorbed by more employees, leading to fewer financial risks.

- Location of your business: Major cities and areas prone to disasters tend to have higher costs.

- Type of coverage: How much you pay depends upon the coverage you select. Higher limits and comprehensive plans that cover preventive care lead to increased premiums.

- Age of Employees: The age of your employees can also affect how your monthly premium. Older employees may be more expensive to insure than younger, healthier employees.

Business claims history: Small businesses with high claims may have to pay higher premiums.

Yes, small businesses may qualify for the Small Business Health Care Tax Credit, which covers up to 50% of premium costs for employers who provide health insurance to employees.

Eligibility criteria for the credit are included in the guidelines released by IRS.

{kind=link}

{kind=link}